Waves of Structural Globalization since

1800: New Results on Investment Globalization

Christopher Chase-Dunn, Andrew Jorgenson, Rebecca Giem,

Shoon Lio, Thomas E. Reifer, and John Rogers

Institute for Research on World-Systems

https://irows.ucr.edu

College Building South

University

of California-Riverside

Riverside,

CA. 92521-0419

chriscd@mail.ucr.edu

To be

presented at the annual meetings of the American Sociological Association,

August 16-19, 2002,Ā Chicago. This

research is supported by the National Science Foundation, Sociology Program. Draft

v. 8-14-02. words=8153. Thanks to Carol Bank and Siobhan Tuthill for their help

with this research. This paper is available at https://irows.ucr.edu/papers/irows10/irows10.htm

To be

presented at the annual meetings of the American Sociological Association,

August 16-19, 2002,Ā Chicago. This

research is supported by the National Science Foundation, Sociology Program. Draft

v. 8-14-02. words=8153. Thanks to Carol Bank and Siobhan Tuthill for their help

with this research. This paper is available at https://irows.ucr.edu/papers/irows10/irows10.htm

This paper discusses research that is designed to examine

the historical trajectory of structural globalization as an attribute of the

whole world-system. Did the globalized world economy arrive all at once in a

rapid and recent transition from national to global economic networks? Or is

the process of international integration a long-term trend that has been going

up for centuries only to be noticed recently because it has reached such a high

peak?Ā Or, alternatively, is globalization

a cyclical phenomenon in which the world-system alternates between periods of

national autarchy followed by periods of international economic and political

integration?ĀĀ

We propose a conceptualization

of structural globalization as several inter-related dimensions of the

expansion and intensification of interaction networks. The real trajectories of

different kinds of globalization over the last two centuries are knowable only

if we gather comparable data over time.Ā

Studies of recent decades do not answer the question of the shape of

long-term trajectories.Ā Our project

improves upon data for the nineteenth century and splices earlier, cruder

measures with later, more refined and more complete data series.

The two main objectives of our

research are:

Ę to

determine the trajectories of trade and investment globalization; and

Ę to

empirically examine the relationship between these and several other

world-system variables that have been hypothesized to cause international

economic integration.

The trajectories of different types of globalization have

important implications for our understanding of the processes of development in

the modern world-system. In this paper we present new results on the trajectory

of investment globalization.

ĀĀĀĀĀĀĀĀĀĀĀ Both the popular and the academic

discourses about globalization contain great confusion and disagreement

regarding the meaning and connotations of this contested term. We contend that

the scientific study of globalization can move forward by making a clear

distinction between globalization as greater integration and interdependence of

the world-system, on the one hand, and the political discourses that employ

ideas about global integration and competition to justify actions and policies

on the other. Our research will distinguish between:

Ę

globalization as ideology, and

Ę

globalization as objective structural trends of spatial

integration.Ā

Our main focus is on different types of structural

globalization, but we are also interested in understanding changes in the

ideologies that are used to legitimate the actions of the powerful. Giovanni

Arrighi is researching the transition from Keynesian theories of national

development to the neo-liberal ōWashington Consensus.ö Phillip McMichael (1996)

describes the emergence of what he calls the ōglobalization projectö ¢ a

revitalized glorification of market mechanisms as allegedly efficient antidotes

to rent seeking and the ōvampire state.öĀ

The ōglobalization projectö emerged with Thatcherism and Reaganism in

the 1980s, and has swept around the world as a justification for attacking and

dismantling welfare states and labor unions following the demise of the Soviet

Union. While this is an interesting and consequential phenomenon, it is not to

be the main focus of the research here proposed.

ĀĀĀĀĀĀĀĀĀĀĀ Rather we intend to determine

the real temporal trajectories of structural dimensions of global integration

over the past two hundred years. We understand structural globalization as

composed of different inter-related dimensions of expanding and intensifying

interaction networks ¢ especially political, economic and cultural

globalization (Chase-Dunn 1999).Ā We

specifically reject the notion that these dimensions constitute completely

different aspects of social reality that should be studied separately by

different academic disciplines, but we contend that it is useful to distinguish

between them in order to understand how they have affected one another.

Our research has already shown

that trade globalization is primarily a cyclical phenomenon, though the most

recent upsurge has reached a level that is significantly higher than the level

reached at earlier peaks (Chase-Dunn, Kawano and Brewer 2000).Ā In the future we propose to determine the

trajectories of:

Ęinvestment

globalization ¢ the extent to which international capital flows and

investmentsĀ increase (or decrease) in

relationship to the size of the world economy; and

Ę

political globalizationĀ -- the degree

to which the multicentric international system has moves toward centralization,

integration and hierarchy.

The quantification of political

globalization will require measures of the relationship between the power and

sizes of large and small political and military organizations in the

world-system. We propose to operationalize these characteristics of the whole

world-system over the past 200 years in order to compare their temporal

trajectories with that of trade globalization, and to examine their

hypothesized causes.

ĀĀĀĀĀĀĀ We

define structural globalization as the

increasing spatial scale and intensity of interaction networks. Charles

Tilly (1995:1-2) proposes a similar definition of globalization as "an

increase in the geographic range of locally consequential social interactions,

especially when that increase stretches a significant proportion of all

interactions across international or intercontinental limits." If both

national level and global networks increase in intensity at the same rate, this

approach would not see an increase in the globalization of interaction.Ā Globalization in the structural sense is

increasing integration and interdependence. As with other efforts to

measure globalization (e.g. Chase-Dunn, Kawano, and Brewer 2000), the

estimation of a global characteristic needs to take account of the changing

size of the system as a whole.Ā Of

course there are more transnational interactions now than there were in the

nineteenth century.Ā There are also more

within-nation interactions because the world population and the world economy

have become larger.Ā It is the ratio of

these that must be studied.

Human interaction networks have

been increasing in scale and intensity for millennia as transportation and

communications technologies have made regular trade and interaction over

greater distances possible.Ā It is obvious

that the railroad and the steam ship facilitated a massive increase in the

spatial scale of interaction networks.Ā

Ideally we would like to trace the relative degrees of interaction

integration at several levels.Ā

Households exchange goods and ideas with other households. Neighborhoods

and towns exchange with other neighborhoods and towns, cities with cities and

etc.Ā But such a study is not feasible

at the present for two reasons: our unit of analysis is the world-system as a

whole ¢ meaning all the countries of the world; and we want to examine trends

over the past 200 years.Ā It might be

possible to examine local and regional interaction networks for a particular

country or for a few core countries in recent decades. But in order to study

the whole system over two centuries we must necessarily use data on the units

that have been the main data-gatherers in this period of human history ¢ the

national states.

ĀBy this decision we do not mean to imply that national states are

the only, or even the most important, actors in the world-system. We recognize

the importance of transnational relations emphasized by political scientists

thirty years ago (Keohane and Nye 1970; and more recently by Sklair (1995,

2001).Ā The world-systems perspective

has long pointed out that the interstate system ¢ the system of sovereign

national states -- is only one institutional structure of the global political

economy.Ā The world-system is composed

of individuals, households, towns, cities, regions, firms, classes, states, and

other non-governmental and international organizations.Ā It is not simply a matter of ōinternational

relations.ö The world-system is the whole

system, not just relations among states.Ā

Transnational relations occurring across state boundaries between all

these social actors are not a new, or a recent, phenomenon.Ā Intersocietal migrations and trade among

individuals, families and firms have been important aspects of small, medium

and large world-systems for thousands of years. There was never a time in which

the members of different societies did not importantly interact with one

another (Chase-Dunn and Hall 1997).Ā But

the spatial scale of both societies and intersocietal interactions has grown.

And intersocietal integration only became global in the sense of linking every

region of the Earth into a single network in the nineteenth century.Ā The unit of analysis we will study in this

research is the modern Europe-centered system as bounded by the system of

allying and conflicting states. It was during the nineteenth century that the

states systems of East Asia and Europe became linked by political/military

interaction, though they had long been linked by the exchange of prestige

goods..

If we think of the world

economy as a system the phenomenon of globalization should represent increases

in the intensity of global interaction networks relative to the intensity of

local interaction networks.Ā If both

local and global interactions increase at the same rate it would be mistaken to

say that the system is becoming more globalized.Ā It is when global interactions increase at a greater rate than

local interactions that the system qua

system is more integrated at the global level. In order to study globalization

in this sense we need to measure the intensity of both global and local

interactions.

ĀThis study will focus on variable characteristics of the

world-system as a whole.Ā The questions

we are asking here are about the continuities and changes at the level of the whole

system, and so our empirical strategy will be to construct measures of how this

single larger system changes over time. For this reason we have only one

ōcase,ö though we can utilize the method of time series analysis to test

propositions about the relationships among variables in this single case

(Chase-Dunn 1998:Chapter 15).

ĀĀĀĀĀĀĀĀĀĀĀ Internationalization

of finance and investment, the growth of international trade as a proportion of

all economic interaction, and the organization of production on a global scale

by transnational corporations have undoubtedly increased in the last two

decades. There are potentially a large number of different indicators of

economic globalization and they may or may not exhibit similar patterns with

respect to change over time.

Ā

Trajectories of Trade and Investment Globalization

We have constructed an improved

measure that shows that there have been three waves of trade globalization

since the early nineteenth century.Ā Our

new measure of trade globalization extends yearly data further back in time and

greatly improves the time resolution relative to the widely spaced estimates

that had been previously available. Our new measure of ōaverage opennessö trade

globalization estimates the world level based on averages of country ratios of

GDP to imports.Ā Because both GDP and

imports are available in country currencies (e.g. francs, pesos, etc.) we are

able to estimate trade globalization without resorting to the problematic

assumptions involved in converting country currencies into a single currency

(e.g. U.S. dollars), and we did not have to convert the current values into

constant values using estimates of inflation and deflation.Ā The results of our study was published in

the American Sociological Review

(Chase-Dunn, Kawano and Brewer 2000).[1] Our

study of trade globalization shows that it is a cyclical phenomenon, as well as

containing a long-term upward trend based on the comparison of the peaks of the

cycles (see Figure 1).

Figure

1: Average Openness Trade Globalization, 1830-1992 (Weighted)

ĀIt is possible that investment globalization behaves in a similar

way, but we do not know for sure. Existing estimates of investment

globalization (e.g. Bairoch 1996) are even more intermittent than estimates of

trade globalization were before we undertook our ASR study.Ā It would be

desirable to have a better understanding of the relationship between investment

and trade globalization and to be able to study the causes of both.

The Trajectory of Political Globalization

ĀĀĀĀĀĀĀ We

conceptualize political globalization analogously to our understanding of

economic globalization as the relative strength and density of larger versus

smaller interaction networks and organizational structures.Ā Much has been written about the emergence

and development of global governance and many see an uneven and halting upward

trend in the transitions from the Concert of Europe to the League of Nations

and the United Nations toward the formation of a proto-world state. The

emergence of the Bretton Woods institutions (the International Monetary Fund

and the World Bank) and the more recent restructuring of the General Agreement

of Tariffs and Trade as the World Trade Organization, and the visibility of

other international fora (the Trilateral Commission, The Group of Seven

[Eight]; the Davos meetings, etc.) support the idea of emerging global

governance.Ā The geometric growth of

international non-governmental organizations (INGOs) is also an important

phenomenon of global governance and the emergence of global civil society

(Murphy 1994; Boli and Thomas 1999).

ĀĀĀĀĀĀĀĀĀĀĀ All

world-systems go through cycles of political centralization and

decentralization with occasional leaps toward new and higher levels of

political integration (Chase-Dunn and Hall 1997). In the modern world-system

the cycle for the last 400 years has taken the form of the rise and fall of

hegemonic core states. Some claim that this hegemonic sequence is now morphing into a new structure of core

condominium (Goldfrank 1999).Ā We intend

to study both the hegemonic sequence and emerging global governance. While

these might be combined into a more general concept of political globalization,

we contend that it is important to keep them separate because hegemonic rise

and fall is an old feature of the world-system, whereas political globalization

is arguably much more recent.Ā Political

globalization can be analytically reduced to the question of the relative

strength of larger vs. smaller political and military organizations (including

also the functionally ōeconomicö ones (IMF, World Bank, WTO) mentioned above.[2].

There is a single size

distribution of political/military organizations in the world-system. We plan

to operationalize three different parts of this size distribution, as well as

the whole thing.Ā Our conceptualization

of political globalization will be analogous to our understanding of economic

globalization ¢ a ratio of the size and importance of global and international

organizations vs. the sum of size and importance of national (and

multinational) states.Ā But we will also

operationalize the hegemonic sequence by examining changes in the distribution

of economic and military power among the core states using the research of

Modelski and Thompson (1996).Ā And we

will study the changing shape of the whole system of states as well, taking

into account the processes of colonization and decolonization (Bergesen and

Schoenberg 1980), the incorporation of the peripheral and semiperipheral

regions into the interstate system, and changes in the distribution of economic

and political/military power in the whole system of states.Ā We will also combine political

globalization, hegemonic rise and fall, and state power stratification into a

single overall measure of the distribution of power among state and proto-state

institutions. This latter we will call ōoverall global political/military

inequality.öĀĀ

Measuring Investment Globalization

We have assembled an annotated

bibliography on sources of information about international investments since

1800.[3] In

principle, investment globalization is the proportion of all invested capital

in the world that is owned by non-nationals (i.e. ōforeignersö).Ā In practice we cannot easily measure the sum

total of all invested or loaned capital (or the amount of domestically owned

capital) over the desired time period, so we use the total of all the national

GDPs to estimate the economic size of the world economy. World GDP will serve

as the denominator of our ōworld totalsö estimate of investment globalization.

The numerator will include

most, but not all, international capital flows, ownership claims and debts. We

will not include transfer payments made by individuals to their families in

other countries because these are not economic investments of the kind we want

to study. We do not include payments for imported or exported goods -- these

are the basis of our measure of trade globalization. Nor do we include foreign

reserves held by central banks in order to support their currencies in the

world money market.Ā But we do include

loans and direct equity investment, profits (repatriated or not) and intrafirm

transfers that cross state boundaries regardless

of whom the parties to the

transactions are.Ā The transacting

parties may be individuals, firms, banks or governments.Ā In principle we want to measure all of the

international financial transactions that involve claims of ownership,

control or debt irrespective of who the parties are.Ā And ideally we would like to systematically

distinguish among these different kinds of international capital flows and

obligations to see how they are similar or different in their geographical and

temporal distributions.

This latter desideratum will

only be possible for the period after World War II. Before that we will find

different combinations of the several types of international capital flows and

obligations in the available data and we will need to be careful about how we

combine and splice data series that contain different components.Ā For example, for early periods it will be

easier to get data on loans made to governments, than to find information on

loans made to private firms or individuals within a country.Ā Whenever possible we will continue the less

inclusive measures into periods in which more comprehensive and decomposable

information is available and we will overlap less complete indicators with more

complete ones. This will enable us to splice different data series in a more

sophisticated way than simply switching from one to another as more complete

data become available.[4]

ĀĀĀĀĀĀĀĀĀĀĀ We also

need to pay close attention to the important distinction in international

capital data between stocks and flows. Stocks are the total accumulation

of debts or the book value of foreign investments at a particular point in

time, while flows are the amount of moneys that flowed in (or out) over a short

period, usually one year.

ĀĀĀĀĀĀĀĀĀĀĀ We are

pursuing two different strategies for constructing long-term measures of

investment globalization.Ā These are

loosely analogous to the ōworld totalsö and ōaverage opennessö strategies that

we describe in our ASR study of trade globalization. The first will

involve gathering data on the main investing countries, (e.g. Britain, France,

Germany, the United States, the Netherlands, Belgium and Switzerland) on both

the outflows and the accumulated values of foreign loans and investments. This

is the strategy that has been employed in earlier studies. It assumes that the

great bulk of foreign capital comes from these countries and so efforts are

concentrated where they reap the greatest informational returns.Ā The disadvantage is that the number of

countries with significant capital outflows increases over time and it is

difficult to know how the missing cases might be affecting the estimate of the

value of international capital. This method also requires the problematic

assumptions involved in converting values into a single currency unit for

purposes of comparison of different countries, and converting current into

constant units for comparing over time.Ā

Nevertheless we propose to

upgrade the currently available estimates that use this approach by adding data

from more investing countries.Ā Suter

[1992:Appendix (f)] has compiled the most complete long-run data series on the

value of international capital holdings. We propose to improve upon SuterÆs

compilation by adding data from additional investing countries and splicing the

early series to a series compiled from more complete data after 1950. We will

also disaggregate the ōnetö figures used by Suter whenever possible for the

countries that he did cover.Ā Net figures

are the balance of credits and debits. In most previous studies of changes in

the level of foreign investment net values have been used (e.g. Suter 1992).

The problem here is that a country may have large amounts of capital invested

abroad and large investments from abroad and these will cancel each other when

net values are used. [5]

ĀĀĀĀĀĀĀĀĀĀĀ Our

second strategy is similar to the ōaverage opennessö approach we developed for

studying trade globalization.Ā This will

involve estimating ōinvestment dependenceö for each country -- the ratio of the

foreign debt to the national income (GDP), and then taking the weighted average

of these as our indicator of world investment globalization.Ā The advantage of this approach is that it

does not require converting into a single currency and computing constant from

current values.Ā We already have the

country currency GDPs (national income estimates) from Mitchell

(1992,1993,1995) that we used for our measure of average openness trade

globalization.Ā For our new ōaverage

investment dependenceö measure of investment globalization we will need to

collect estimates of inflows and accumulated stocks and debts of foreign

capital in country currencies for each country.[6]Ā With complete data these indicators would be

equivalent to the total sum of international capital flows and obligations

divided by the world GDP. But as with average openness, we will not have

complete data for the years before 1950. This will be a ōsamplingö problem in

which the sample is biased because we will have more core countries than

peripheral countries.Ā This indicator

will be compared with the results of our first strategy discussed above.

Analyses

ĀĀĀĀĀĀ The first task of analysis will

be to use the new data we have coded on international capital flows and

obligations to construct several new indicators of investment globalization.

Then we will see how these relate to one another and study their temporal

trajectories in comparison to what we have found for trade globalization.Ā We expect that investment globalization will

show a similar cyclical pattern, but it may not. We also will consider the

question of a long-term trend in investment globalization, much as we did in

our study of trade.

At the time of this writing, August 2002, we have coded and analyzed data on non-net British foreign investment flows from 1865 to 1914 that were not available to Suter (Stone 1999), and we have coded several measures of investment globalization from 1938 to 1999. Some preliminary results and discussion of British foreign investment flows in the nineteenth century are included in Appendix below.

Investment Globalization, 1938-1999

These measures are based on credits and debits on investment income coded from the International Monetary Fund Balance of Payments Yearbooks. Investment income includes the repatriated profits on direct investment and dividends on portfolio investment.Ā Credits means that such was earned from abroad. Debits means that investors abroad were paid profits and dividends by their holdings in the country.[7]Ā In principle, if we had data on the whole world, the sum of credits should equal the sum of debits. But of course we do not have complete data until very recent years, so it is useful to compare credits with debits to see how our ōsampleö of countries may be biasing our estimates of this variable characteristic of the whole world economy (investment globalization).

Investment income has been used as a proxy for estimating the total book value of foreign investment, because there is a general profit rate that averages around 10% and so the profit can be used as a proxy.[8] And the amount of profit and dividends produced by foreign investment are also of interest in their own right.

We coded investment income debits and credits for all available countries from the IMF Balance of Payments Yearbooks from 1938 to 1999. We found that the CD ROM datasets made available from the IMF do not always include all the information that was published in the original Balance of Payments Yearbooks and so it is important to use both the printed volumes and the CD ROM.

Our new measures of ōaverage

investment dependence/dominanceö investment globalization estimate the world

level based on averages of country ratios of GDP to credits and debits of

investment income.Ā Because both GDP and

investment income are available in country currencies (e.g. francs, pesos,

etc.) for many countries we are able to estimate investment globalization

without resorting to the problematic assumptions involved in converting country

currencies into a single currency (e.g. U.S. dollars). Exchange rates vary

because of monetary regulation regimes such as the Bretton Woods agreements,

and because of speculative activities of money traders. And we do not need to

convert the current values into constant values using estimates of inflation

and deflation.Ā Removal of the error

introduced by exchange and inflation rates provides superior estimation of

investment globalization.[9]

Another advantage of using the IMF Balance of Payments Yearbook data is

the avoidance of net values. In our analysis of Balance of Payments data we

examine both credits (the returns received by a country for investments

abroad), and debits (the amounts paid out to foreign investors).Ā

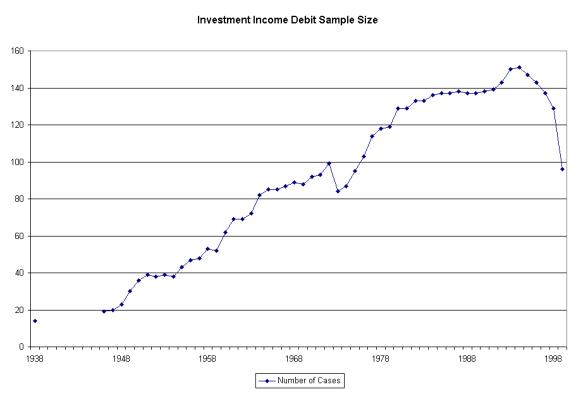

In order to estimate the world level of investment globalization we need to weight the country values. Treating large and small countries equally produces an average that overvalues the information from small countries. We weighted the investment ratios for each country by the ratio of the countryÆs population size to the world population. The weighted and unweighted averages were compared to make sure that our weighting did not produce strange results. The problem is that the ōsampleö of countries upon which we are estimating the world level of investment globalization changes over time. Most usually we have more complete data on core countries than on non-core countries in earlier time periods,[10] but the number of countries does not rise in a nice even trend. Figure 2 shows the changes in the number of countries for which we have estimates for debits of investment income since 1938.

Figure 2: Number of Countries with Debits on Investment Income Data, 1938-1999

Notice that in Figure 2 the number of countries for which we have information on debits on investment income decreases during the 1970s.Ā Researchers at the IMF have been unable to explain to us why the availability of data decreases in that period. Notice also that the data availability decreases after 1995. This is because some countries are tardy in reporting their international financial statistics. The pattern of availability is almost exactly the same for Investment Income Credits.

We present the results of our

study using three different indicators from the IMF Balance of Payments

Yearbooks ¢ total investment income; direct investment income and portfolio

investment income. Total investment income is the sum of direct investment

income, portfolio investment income, and ōotherö investment income. The

definitions of these current account items are as follows:

Investment income covers

receipts and payments of income associated, respectively, with holdings of

external financial assets by residents and with liabilities to nonresidents. Investment

income consists of direct investment income, portfolio investment income,

and other investment income.Ā The direct

investment component is broken down into income on equity (dividends, branch

profits, and reinvested earnings) and income on debt (interest); portfolio

investment income is broken down into income on equity (dividends) and income

on debt (interest); other investment income covers interest earned on other

capital (loans, etc) and, in principle, imputed income to households from net

equity in life insurance reserves and in pension funds (Balance of Payments

Statistics Yearbook, 2001).[11]

We have coded the three subcategories of Investment Income because we are interested in the differences between foreign direct investment and portfolio investment. Direct investment involves organizational control, as when a transnational corporation invests in its subsidiary. Portfolio investment does not involve direct organizational control. The purchase of stocks of firms or of bonds by foreigners is considered portfolio investment. The subcategories are available for many fewer cases and for only recent years. Nevertheless we shall be interested in comparing direct and portfolio investment globalization.

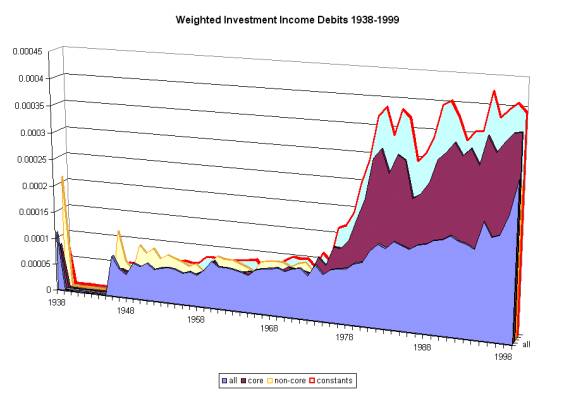

Figure 3 shows the weighted average investment income debit ratios for 1938-1999. Recall that investment income debits include the profits, interest, and dividends earned by foreigners within a national economy.Ā Not surprisingly this estimate of worldwide investment globalization goes up over this forty-year period. But the yearly data enable us to examine the exact temporality of the rise.

Figure 3: Weighted Total Investment Income Debits, 1938-1999

The results in Figure 3 show the averages for all the countries for which we have data (the number of which increases greatly over time as shown in Figure 2), for just the core countries and for the non-core countries.Ā The changes in Figure 3 are partly due to changes in the level of worldwide investment globalization and partly due to changes in the availability of data over time.Ā In order to take out the part due to changing N we use the method of constant groups, looking at a set of countries for which we have data over the whole span of time. In Figure 3 the constant group includes eleven countries ( Australia, Canada, Denmark, Finland, Ireland, Italy, Netherlands, Norway, Sweden, United Kingdom and the United States). The close similarity between the results for the constant group and for the core is due to the fact that the core countries are the ones for which we have the most data further back in time.

The trajectory of investment globalization indicated by including all the countries for which we have data on debits on investment income shows that there was a decrease between 1938 and 1946, and that was followed by a slowly accelerating upward trend. The 1938 level was not reached again until 1979, but the level reached by 1999 was almost three times higher than the 1938 level. Thus the perception that the world economy experienced a wave of investment globalization in recent decades is confirmed by our results using our new ōaverage investment dependenceö estimator based on debits on investment income.

Figure 3 also shows that the trajectory has been rather different for the core and the non-core. In 1938 the non-core countries were more than twice as dependent on foreign investment as were the core countries and the non-core declined from this high level until the late 1950s, while the core began a new ascent from 1946 on. In 1975 the core began a sharp upturn in payments out on investment income, whereas the non-core was experiencing a much slower increase. This indicates that investment globalization occurred much earlier and to a much greater extent for the core countries than for the non-core.

ĀĀĀĀĀĀĀĀĀĀĀ Now let us examine the credit component of investment income. This is composed of the profits, interest and dividends taken in by countries as a result of their investments abroad, a feature we call ōaverage investment dominance.ö Figure 4 shows the weighted trends since 1938 for the same groups studied Figure 3.

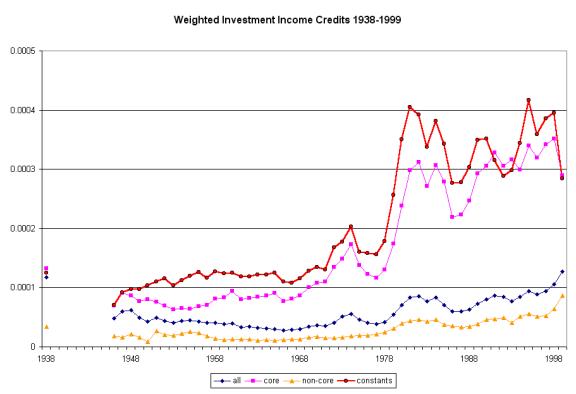

Figure 4: Credits on Total Investment Income, 1938-1999

ĀĀĀĀĀĀĀĀĀĀĀĀĀĀĀ The results in Figure 4 are similar in most respects to Figure 3, except that the upward trend for the whole world and for the non-core countries is much weaker.[12] Credits on investment income have gone up mainly for the core, and this acceleration is temporally similar to the results for core debits shown in Figure 3. The other difference is that core credits were already higher than non-core credits in 1938. This is just the opposite of the pattern for debits. Core countries are the main global investors and this difference between core and non-core has increased over time despite all the talk of emerging markets and transnational corporations based in the semiperiphery.

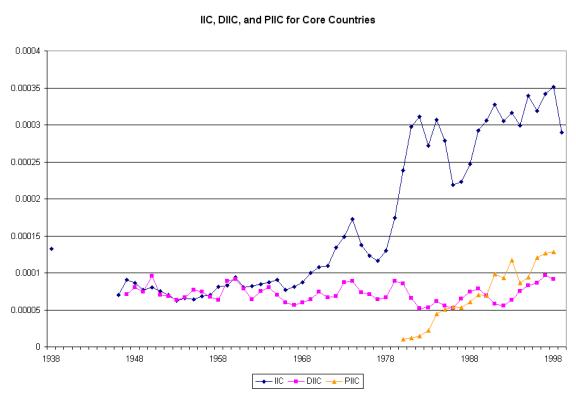

ĀĀĀĀĀĀĀĀĀĀĀĀĀĀĀ Figure 5 compares two of the components of investment income debits with the total investment income debits for the core countries.

Figure 5: Total, Direct and Portfolio Investment Income Debits, Core Countries

ĀĀĀĀĀĀĀĀĀĀĀĀĀĀĀ Figure 5 shows some interesting differences for the core countries across different kinds of investment income debits. The total investment income trajectory is the same as that shown in Figure 3 above. Average weighted direct investment income debits for the core countries do not show an upward trend. The upward trajectory shown by total investment income debits is entirely due to the increase of payments out on portfolio investment and on ōotherö investment income (not shown). [13] ōOtherö investment income primarily includes items that can be considered as parts of international investment. [14] Thus the increase in core investment globalization as indicated by debits on investment income appears to be largely due to the rise of portfolio investments corresponding to the financialization of the world economy that has accompanied the ideological hegemony of neoliberalism since the 1970s. Debits on direct investment income in the core appear to have remained flat relative to the size of the world economy in this period, meaning that the amount of profit paid out by core countries resulting from the activities of subsidiaries of transnational corporations has apparently not increased.

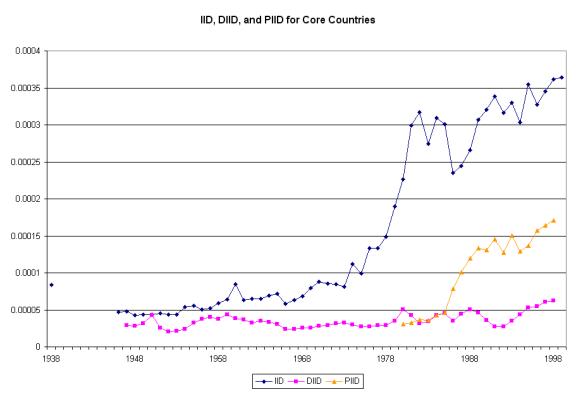

ĀĀĀĀĀĀĀĀĀĀĀĀĀĀĀ Let us now examine the trends for the subtypes of credits on investment income. Figure 6 shows the corresponding credits categories to those shown in Figure 5.

Figure 6: Total, Direct and Portfolio Investment Income Credits, Core Countries

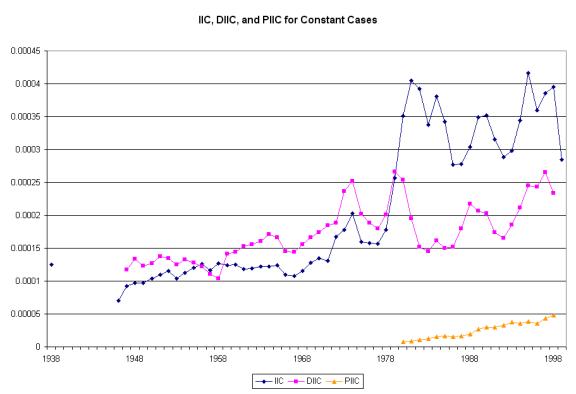

Figure 6 shows a very similar pattern as Figure 5. The trend in total investment income credits for core countries is the same as in Figure 4 above. As in Figure 5, direct investment globalization is flat, while portfolio investment globalization shows a strong rise since the late 1970s. But some of the trend in Figure 6 is due to changes in the cases. Figure 7 shows the results when we hold the cases constant for each of the subtypes.

Figure 7: Credits on Total, Direct and Portfolio Investment Income for Constant Cases

Figure 7 indicates that the flatness of the trend in direct investment credits shown in Figure 6 may be due to the addition of cases as we move through time. When we hold the cases constant, direct investment credits show a modest upward trend.[15]

The conclusions suggested by our study of investment globalization from 1938 to 1999 are as follows: there was indeed an upward trend of investment globalization during this period but it began after a decline during World War II. The big rise began in the late 1970s corresponding with the abandonment of the Bretton Woods regulations over international investment and the deregulation of international monetary arrangements. There were important differences between the core and the non-core with regard to investment globalization. The core did it earlier and rose to a much higher peak. Portfolio investment was a major contributor to the big wave of investment globalization that occurred after the late 1970s. This corresponded to the shift of capital accumulation away from investment in production and trade and into finance capital.

ĀĀĀĀĀĀĀĀĀĀĀĀĀĀĀ What remains to be done for this part of our study of trends in investment globalization is to compare our ōaverage investment dependence/dominanceö measures with world totals measures, and to compare our results for investment globalization with yearly trade globalization figures and with other types of globalization. We also need to finish linking our study of nineteenth century investment globalization with the post-1938 measures, splicing the series in a way that permits us to address the questions of cycles and long-term trends that motivate our comparison of the nineteenth century wave of globalization with the twentieth century wave. How big is the upward trend? What is the precise temporality of investment globalization and how does it relate temporally with other types of global integration? Which kinds of integration lead and which ones lag? What causes global integration and what does it cause? And how can our study of global integration help us lower the probability of future conflicts and increase the probability of global cooperation, stability, democracy and equality.

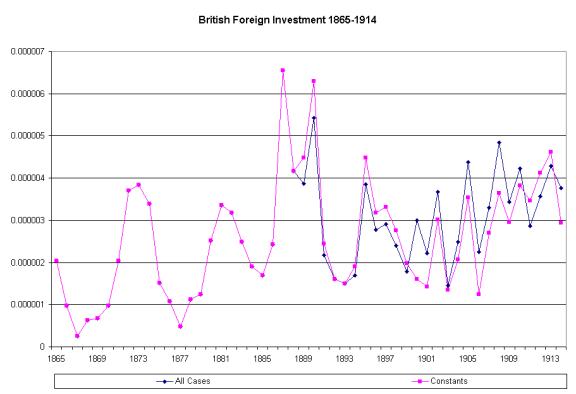

Appendix A: Yearly Non-net British Foreign Investment Flows,

1862-1914

ĀĀĀĀĀĀĀĀĀ Our best yearly estimate so far of investment globalization in the nineteenth century comes from Irving StoneÆs (1999) new study. This is a much-improved basis for estimating the trajectory of investment globalization in the nineteenth century because it does not rely on net figures. We have used StoneÆs estimates of total private capital exports (flows) from the United Kingdom to thirteen countries (Argentina, Australia, Canada, Chile, Germany, Spain, France, India, Italy, Japan, Mexico, United States and South Africa) in pounds stirling and national income estimates in country currencies (converted into British pounds using exchange rates). These have then been weighted by the ratio of the countryÆs population to the world population and then the average for all the countries available for each year have been calculated with Figure 8 as the result.

Figure 8: Investment Globalization Based on British Private Capital Exports, 1865-1914

ĀĀĀĀĀĀĀĀĀĀĀ The method used in Figure 8 to produce yearly estimates of investment globalization is based on flows, the average amount of capital exported from Britain each year rather than on estimates of the total book value of British capital within each country. This may contribute to the volatility of the values, but the upward and downward trends seem to track the ten-year business cycle fairly closely. Interestingly the Great Depression that began in 1873 initiated a fall of capital exports that was no deeper than the previous decadal downturn, and in 1885 a steep ascent began that reached the highest peak of the whole period. From these data it appears that investment globalization has a similar trajectory to that of trade globalization in the nineteenth century. Recall that the trajectory of trade globalization in Figure 1 above has been transformed by a five-year moving average that smooths out short-term variations.

ĀĀĀĀĀĀĀĀĀĀĀ We are not satisfied with this measure of nineteenth century investment globalization for several reasons. First, the United Kingdom was perhaps the most important investing country, but rather important foreign investments were also flowing from France, Belgium, Germany, and after 1900 from the United States. The other big problem is that these yearly export flows do not provide good estimates of the total value of foreign-held assets in the countries to which they are flowing. The way to estimate the total value of capital is to sum current investments over a period of years depreciating the earlier years with an amortization schedule. This is our next step for the British flow figures, and these will need to be weighted by estimates of world GDP. To accomplish this latter we will need to transform MaddisonÆs (1995, 2001) estimates from 1998 Geary-Khamis U.S. dollars into current British pounds for the nineteenth century (or transform current pounds into 1998 Geary-Khamis U.S. dollars). This will provide a better estimate of nineteenth century investment globalization that the flows numbers shown in Figure 8.

Appendix B: List of Core and Non-core Countries Studied

with IMF Balance of Payments Data.